By using an account aggregator rbi (AA), a particular type of RBI-regulated company (with an NBFC-AA licence), an individual can securely access and exchange information between one financial institution with which they have an account and any other regulated financial institution in the account aggregator framework RBI network. Nothing about the person may be shared without the person’s permission. One can choose from a variety of account aggregator framework RBI options. RBI, the account aggregator, replaces long-term “blank check” type approvals with detailed, step-by-step consent and controls for every use of your data.

What does RBI’s account aggregator framework consist of?

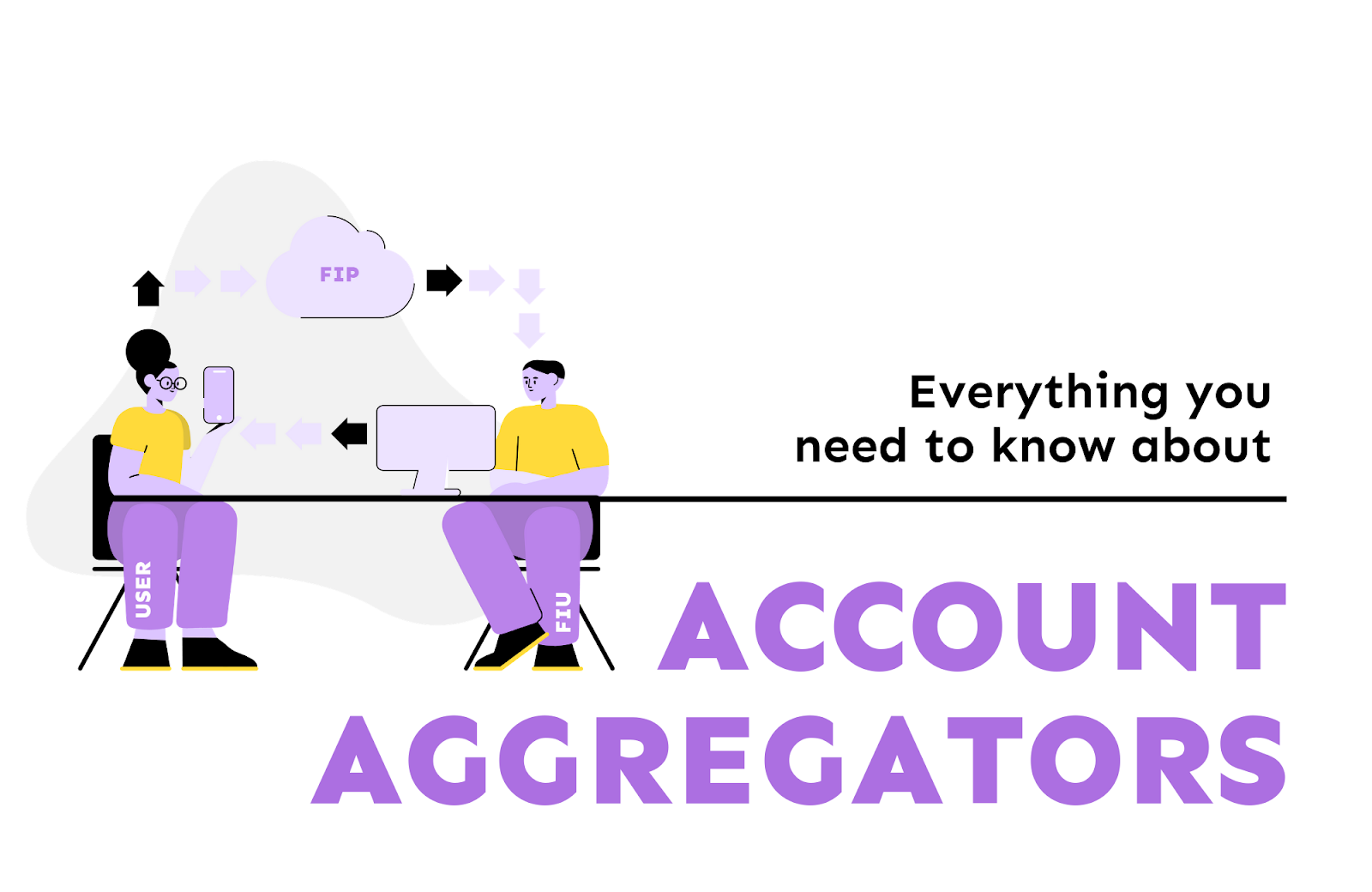

The real-time exchange of financial data across regulated organisations is made possible by the ecosystem of account aggregator architecture provided by RBI. The four major financial regulators—the RBI, IRDA, PFRDA, and SEBI—joined forces to allow regulated businesses under their oversight to exchange data with account aggregator RBI after receiving user consent.

How would the new Account Aggregator network benefit the average person’s financial situation?

Consumers in India currently have to deal with a number of financial system annoyances, such as exchanging physically signed and scanned copies of bank statements, rushing to notarize or stamp documents, and being required to provide your specific username and password in order to reveal your financial history to a third party. The account aggregator RBI network’s simple, mobile-based, transparent, and secure digital data access & sharing method would take their place and replace them all. This will open the door for additional services including various types of loans.

What comprises Anumati’s services?

Anumati by Perfios AA is an account aggregator RBI that helps you manage the information you have stored with many financial institutions, aggregate that information, and choose with whom to share it. All of this is done within a very secure system that has completed an RBI safety and security audit. Your data is also exclusively accessible by you, so you are free to share it as you see fit. Anu never sees it. Anu can help in the real world in the following ways. Imagine that you are asking for a loan to cover a certain Diwali purchase. The lender need your most recent six months’ worth of bank statements in order to approve your loan.

What options do you have?

- When applying online, you must first download your bank statement, remember the password, upload the statement to the lender’s website, re-enter the password, and hope for a continuous internet connection.

- If you’re not the self-service kind, you would contact a sales representative at his home, verify his identity, and then hand him the printed statement while crossing your fingers that it wouldn’t be unnecessarily photocopied or land in the wrong hands.

- You may also look up Anu, immediately link your bank account or accounts, and then, in three steps, retrieve and transmit information with the lender through your bank. Within a few seconds. The process is 100 percent safe and secure because there is no “man in the middle” or time lost downloading from one website only to upload at another.

The same way that UPI has made life easier for us—even for little payments to street vendors for 100 rupees.

Here are a few more details about Anumati:

Anumati, a consent manager and account aggregator, is offered by Perfios Account Aggregation Services Pvt. Limited under the RBI licence. All of your bank accounts are listed on Anumati’s simple, user-friendly interface, which also lets you choose with whom to share your financial information and monitors the data collection process on a regular basis. You have the right to modify, renew, or withdraw your consent at any time (this could affect how you communicate with a potential lender). Anumati can safely access your data and then provide it to approved banks. Everything is done in secret and out of sight of the public. Nobody—not even Anumati—can access your data or utilise it in any other manner. Your data is safeguarded, secure, and safe.

How do you start?

Anumati provides a simple three-step process to start helping you:

Sign up – Enter the phone number you’ve registered with your bank and set a 4-digit secret PIN. Anu will send an OTP right away to confirm the mobile number. After verification, your account will be enabled with [Your mobile number]@anumati as your handle.

Find and add bank accounts: Anumati searches for and locates every banking account associated with your mobile phone. Simply select the accounts you wish to link in your account aggregator RBI (AA). If you would like, you can manually add more accounts from the partner banks and financial organisations.

Manage consent- The lender will ask you to provide your financial information via a variety of channels, including Anumati, when you submit an online loan application. Accept carrying out this via Anumati. Customers whose banks have joined the AA network for data sharing, what new services are accessible to them?

What new services are provided?

The two key services that will be improved for an individual are access to loans and access to money management. In order to be approved for a small business loan or a personal loan today, a consumer must submit a number of documents to the lender. Obtaining a loan and accessing one takes longer because the process is currently manual. Similar to how managing money is challenging today since data is scattered across many locations and is difficult to compile for analysis. Framework for account aggregators RBI simplifies the loan application process, enabling companies to easily and affordably access secure, tamper-proof data and assist customers in obtaining loans.

Where does it not work?

As already indicated, Anumati works with most of the big banks and financial institutions. To welcome them as partners, we nevertheless constantly reach out to other organisations. One such company is the State Bank of India. The team is in talks with SBI, so maybe this public sector bank can be welcomed to their network soon. Eventually, they want to add securities companies as well. This is currently being worked on and will be activated as soon as feasible.